Software Development Metrics That Matter to Business Leaders (With Examples)

Tracking and reporting key metrics is paramount to ensuring the success of your software development project. Understand these benchmarks to improve...

Updated January 2, 2025

Businesses shouldn’t assume that blockchain is a blanket solution for any challenge they might be facing. Instead, businesses should carefully examine whether blockchain is the right choice for them and consider their options when it comes to blockchain networks.

Updated 05/06/2022

Blockchain technology’s most well-known application, Bitcoin, recently turned 11 years old. In the last decade, the technology experienced a period of transformation, growth, increased hype, and dramatic falls. Now, it appears to have entered a phase of practical reflection.

Looking for a Software Development agency?

Compare our list of top Software Development companies near you

It is a mistake to assume that blockchain technology is universal. The massive closure of initial coin offering (ICO) projects that raised considerable funds during 2017, for example, shows that blockchain cannot solve all existing problems.

However, it can bring additional value and accelerate the development of industries struggling to build trust with users, such as in finance, the transfer and storage of digital assets and property rights, and the supply chain.

This article is a brief guide to assessing the appropriateness of using blockchain, as well as an overview of the most popular networks that exist on the market.

There are three main considerations to make when selecting a blockchain network to use. Here are our recommended steps:

Need assistance starting up your project? Connect with a leading blockchain company on Clutch.

Before deciding to implement a blockchain in your project, consider if it’s the right solution to the challenges you’re trying to overcome. Blockchain can be complicated, and it's not right for everyone. If it doesn't look like it'll pay off in the long run, consider a different solution.

How do you know if blockchain is right for you? A good place to start is with the following questions:

Blockchain is applicable when there are a certain number of companies or individual participants, and the interaction between them takes place in a completely untrusted environment.

This can be a group of companies competing among themselves or branches of a large company that deliberately spread the nodes of its blockchain into independent units. The main thing is the distribution of security risks among all participants.

If this doesn’t apply to your company, then it is better to use a regular database with good public cryptography.

Blockchain nodes optimize computing resources in order to prevent flooding and network congestion. Thus, in order to avoid this, each transaction should be paid by the user.

Problems with payment of transactions are solved, but not by the cancellation of payment, but by additional functionality that allows some participants to pay for others.

Typically, it is offered one-time and only to new users of the blockchain to facilitate onboarding, but the owners of the system will have to deal with commissions for each transaction in any case.

“Settlements” are not only payments but also any other exchange of digital values. This can be reputation points and information that allows you to access valuable resources.

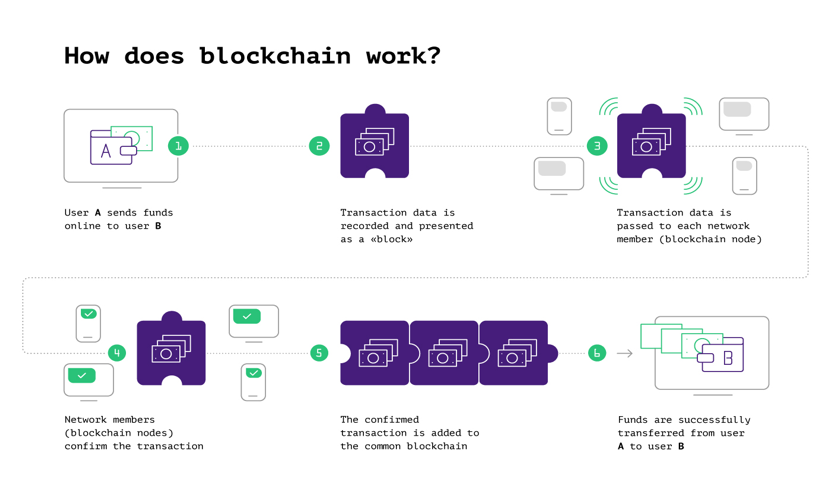

Blockchain networks provide the exchange of digital rights from one account to another without the possibility of manipulation by an arbiter.

Someone requests a transaction that is sent to a network of nodes. These nodes validate the transaction and verify those involving cryptocurrency.

Once the transaction has been verified, a new block is added to the network, completing the transaction.

The main function of the blockchain is to protect precisely these “balances” and complex ways of transferring them between different addresses.

After deciding to use blockchain, you need to understand which blockchain is needed. If you just need to accept payments in cryptocurrencies, choose any of the existing public networks.

But if your project wants to automate more complex operations, you can either choose existing public networks with smart contracts functionality or build your own blockchain with the necessary logic.

Public blockchain: completely open and decentralized blockchain — any individual on the network can participate in transactions. Think of blockchains like Bitcoin, which are open to the public and praised for decentralization.

Private blockchain: access and participation is limited to certain individuals — activity is monitored and under the control of an operator that can make edits to activity on the blockchain.

Permissioned blockchain: blockchains that contain elements of both public and private blockchains. These blockchains are only accessible to individuals with permissions and activity is still limited to verification by administrators.

To work on public blockchains, you do not need to prepare any other code except for smart contracts and the main code of your service that communicates with the blockchain network.

Here are some perks of public blockchain options:

The following are drawbacks to investing in a public blockchain:

Smart contracts are written as code and regulators can watch contract activity on the blockchain to understand it while maintaining privacy.

In fact, you only have interfaces on your computer, and processing is paid by the customers themselves. Therefore, owning a smart contract system is cheaper than a centralized database - You do not need to rent a server, backup, pay for the administrator, or be responsible for the security of user accounts.

Public blockchains are most protected from large-scale attacks. If your project operates on a public blockchain it will not shut down; validators and miners are participants who run the nodes of the blockchain network that support the network’s maintenance and replicate the data.

The drawback of using the public blockchain is the need to pay fees for transactions and having little control over the network itself.

You will not be able to influence the public blockchain network’s course, speed of transaction processing, or which validators/miners are assigned.

Also, at the moment, the scalability of the first generation of blockchains does not allow to process of many parallel operations from tens and hundreds of thousands of users.

Public blockchains are suitable for projects that require “unsinkability” in any conditions, and with sufficiently valuable deals so that users are willing to pay for each operation

If the functionality of any of the public blockchains does not suit you, You can launch it by your own efforts or use frameworks to deploy permissioned blockchains with customizable logic.

To start your own blockchain, in addition to its own code, you must prepare the following integral parts:

You need to collect and motivate a group of people who will set up specific hardware and software to maintain blockchain network ensuring its security and existence in a decentralized and distributed fashion.

These people are the validators/miners. They form the first block of your blockchain, jointly launch the test network, debug all the code update procedures and manage the validators/miners in it.

Only after this is the blockchain ready to launch the main network.

This approach involves a lot of money and time.

Which of these existing blockchain solutions is best? There are a lot of options, so it is important to choose carefully.

What are the main blockchain networks? Here are 5 recommended existing solutions:

We will describe the most reliable solutions that already fulfill the following requirements:

Any of these solutions may be good choices and allow for an ease of implementation that will carry your project toward success.

Ethereum is the most mature and universal proof-of-work solution that allows you to build smart contract systems of great complexity.

Ethereum has the most developed ecosystem, plus convenient and developed languages for writing smart contracts, many tools, and ready-made algorithms.

Also, in case of any problems, data and smart contracts can be transferred from one Ethereum network to another as long as it is Ethereum-based such as PoA Network or Loom Network.

The technological stack for the development of Ethereum is the Rust and Go programming languages.

Currently, Ethereum is an absolute fin-tech leader that allows you to:

Ethereum is a proven leader in the market that investors should seriously consider as a solution for their business needs.

EOS is a fast public blockchain that also supports full-featured smart contracts, the most developed of the blockchains using consensus like “Delegated proof-of-stake” (DPoS).

In EOS, transaction processing speed is high, blocks appear once every half a second. EOS allows you to write smart contract systems of any complexity, has a convenient account system and a voting system for validators.

EOS is well suited for games and gambling, and it can also be used to successfully organize an untrusted network between various IoT devices. It can also serve a payment network of terminals, ATMs, or cryptomats.

The Hyperledger family of blockchains is a system originally designed for corporate use.

Modern projects on HL do not have an internal economy and are usually used as permissioned blockchains for internal workflow in large companies

HL and Fabric, its most successful branch, was created considering the needs of corporate clients. Therefore, many mechanisms inherent in blockchains designed to work in an untrusted public are absent.

Use HL if you need powerful logic and you are ready to run your blockchain inside the corporate network since you can set these networks to public only in read-only mode.

Parity is one of the largest blockchain development companies in the world as a developer of Ethereum, Bitcoin, and a huge number of various blockchain-oriented software.

Substrate is a blockchain constructor framework that allows you to quickly and easily assemble your blockchain, which it refers to as parachain, and run it with its own validators and its own logic.

Using solutions like Substrate and Polkadot is the fastest and most reliable way to create your own blockchain without making mistakes in consensus and transaction processing.

Cosmos SDK is a software package similar to Substrate for building custom blockchains with arbitrary logic, built on the basis of Tendermint consensus.

Cosmos SDK has differences from Substrate, but the general idea remains the same: Instead of placing smart contracts on a public network, this framework allows you to launch your blockchain with the necessary logic, consensus, and anything else.

The main Cosmos chain will allow many of these blockchains to communicate with each other and fix their status in the main chain. During development, the Go language is used, and there is also a large number of ready-made software to support developed blockchains.

Choosing the right blockchain is currently limited mostly to three main blockchains and their forks:

These projects are mature enough with a proven track record so that you can build production-ready solutions.

Make sure alternative blockchains have successfully implemented user cases.

If you choose to work on a public blockchain, you will be able to save costs associated with customization.

If you decide to develop your own blockchain, be ready for the cost and difficult process ahead.

Blockchain technologies are extremely specific and have many internal nuances. Therefore, it is recommended that you carefully consider how the blockchain will be used in your project, what will be the cost of owning such a system, and what it will cost users.

Software researcher, developer, team lead, lecturer, security specialist. More than 25 years of development experience in many languages from Assembler to JavaScript, and infrastructure from low-level software (antiviral analyzers, high-loaded microservices) to bigdata infrastructure for petabyte-scale tasks. Solid background in infosec, high-loaded services, system architectures, cryptography, and algorithms. Co-founder of blockchain development company MixBytes.

See full profile