Is Your Phone Spying On You? (And How to Stop It)

Do you worry your phone is spying on you? You’re not alone. Learn how smartphones collect your data and what you can do to reduce what you share.

Updated June 26, 2025

Blockchain adoption is expanding globally, increasing customer loyalty and changing the customer loyalty narrative in more ways than one.

Updated August 15, 2022

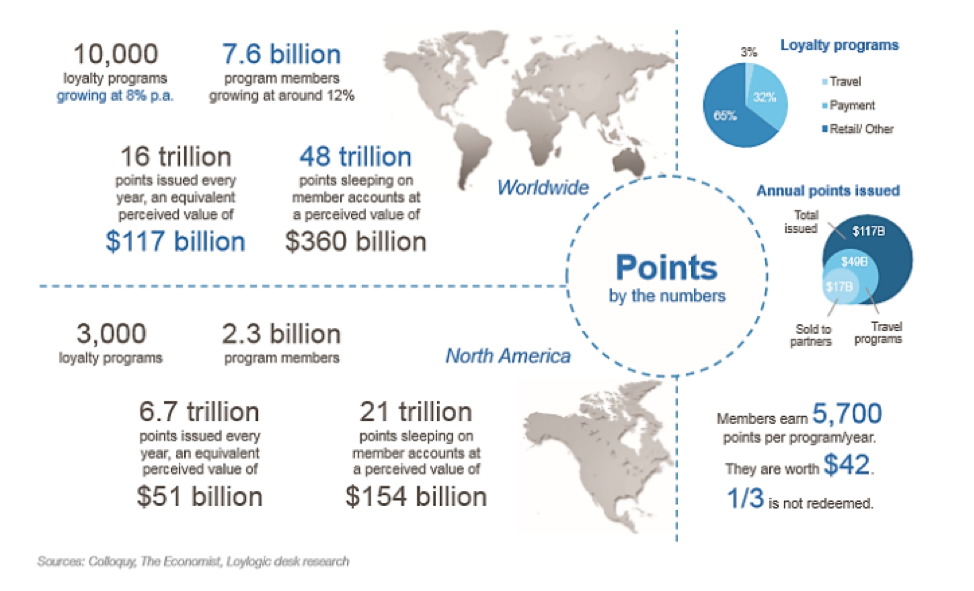

At the time this article was written in 2019, loyalty programs were a huge $360 billion-dollar industry, with more than 16 trillion loyalty points issued annually across 7.6 billion consumers.

Looking for a IT Services agency?

Compare our list of top IT Services companies near you

Rewards programs are a substantial industry that businesses use to drive customer spending and loyalty.

Although loyalty programs are substantial, they are also fragmented; there are too many loyalty programs, each with its own way of earning and redeeming. This can lead to frustrated customers and a lot of unused points.

According to a Colloquy study, the average American is enrolled in at least 29 different loyalty programs. Approximately 50% of these loyalty programs are inactive, and 30% of customers never redeem a single reward point.

Most loyalty programs are very limited, discouraging customer engagement and focusing on centralization. Customers can usually only redeem points with the same retailer they earned them from. Placing limitations on how and where to spend points decreases the loyalty program’s overall value for loyal customers.

Companies can decentralize their loyalty programs through blockchain and capitalize on blockchain technology benefits.

Here are 5 ways blockchain technology or blockchain rewards programs can benefit customer experience and loyalty:

When companies offer more than one loyalty program, it can be difficult to manage for both the company and its customers. The lack of a streamlined customer loyalty program results in missed opportunities, wasted rewards points, and frustration.

A Forbes article explored applying a blockchain-powered system using a single digital coin across many brands or companies, such as bitcoin. This decentralized approach makes the loyalty program easier to manage and track, saving time and giving the customer more value.

This approach gives customers more flexibility and choice, which encourages them to spend more. Although effective, this approach is not suitable for all businesses – outsourcing loyalty programs can get expensive if managed independently.

This approach is best suited for larger companies, conglomerates (such as Banana Republic, Gap, and Old Navy), or companies that enter into a strategic partnership with other brands from a complementing industry (e.g., an airline company, transportation company, and a hotel chain).

These larger e-commerce companies can rely on digital currency through their loyal customers using digital wallets for payments, coupons, and more rewards that mirror traditional loyalty programs.

While startups might not have the resources to rely on digital assets, they can think creatively about the incentives within their loyalty rewards programs. Focus on social media promotion, credit card deals, or cash-back rewards that can make consumers happy for the time being.

Blockchain represents the future and present of some consumer loyalty programs. For example, Singapore Airlines and Delta Airlines recently introduced a blockchain-based loyalty program, replacing their air miles with cryptocurrencies they can use for retail purchases.

If brands are reluctant to make a universal digital loyalty coin with other brands, then they could choose the next best thing – interchangeable coins.

According to a report from Kaleido Insights, the interchangeability of these digital reward coins is a business opportunity for brands.

Blockchain-powered digital coins are far more flexible and interchangeable than loyalty points because they can be treated like currency.

A customer joining these loyalty programs can exchange these loyalty coins into another digital cryptocurrency or money.

This gives people more flexibility on how they would use their digital reward coins, which increases the value of the loyalty program and encourages people to buy more from the brand.

Digital reward coins can even be exchanged for products or services from other brands because the digital coin has value beyond the company that issued it.

The result is a loyalty coin economy that increases in value the more it is used.

Interested in learning about NFTs? Browse our glossary of terms.

Some people are reluctant to join loyalty programs.

Nearly 70% of consumers express concerns, according to a PwC survey, especially when it entails giving away personal information and customer data. This is understandable, with the ever-growing incidents of identity theft online.

Blockchain technology can minimize these risks. Anonymity is a key feature of cryptocurrencies, and customers might not need to give their personal information. Or, if they need to, blockchain can keep the information more secure.

Blockchain’s security features also benefit companies. Nearly 72% of loyalty programs have been misused or ‘cheated’ by people using fake transactions to gain loyalty rewards for purchases they never made.

Records using blockchain are fully transparent and trackable, which makes it difficult for unauthorized transactions to go unnoticed. This makes it harder for people to ‘cheat’ the loyalty program.

Blockchains can minimize the risks of identity theft and fraud, which benefits both the business and its customers.

Loyalty programs are expensive – The cost of tracking points, monitoring redemption, marketing, and calculating the impact on sales adds up. Blockchain is an investment and can help reduce these costs in the long run.

Implementing blockchain becomes easier over time once the processes are in place and partnerships are established.

Blockchain systems reduce costs associated with transaction management, fraud, and system errors.

By investing in blockchain and following the advice of the top cybersecurity consultants, you can give more value to your customers and reduce the costs associated with managing your loyalty program.

Think of new technology as a friend, not a foe.

Some loyalty programs and loyalty platforms are still in the Dark Ages, manually logging points, which takes time and leads to frustrated customers. Blockchain systems make it easier to store and record loyalty point transactions in real-time.

Blockchain is already being used in the food industry to track food products throughout the supply chain. Walmart was able to trace a package of sliced mangos to a farm in Mexico in just 2 seconds by using Blockchain technology, a process that would have normally taken more than a week.

Applying this technology to a customer loyalty program would allow companies to keep track of points in real-time and deliver rewards to their customers more efficiently.

Faster service means more loyal, happy customers.

Hire a financial services provider to look over your company.

The blockchain network can be a useful addition to your company’s strategy.

As blockchain technology continues to disrupt every aspect of business and daily life, loyalty programs are a prime candidate to follow suit. Having faster, smarter, and more flexible loyalty programs can make for increasingly happy customers.

Browse our directory of blockchain solution providers to find a company to set up your loyalty network.

Additional Reading:

Stevan Mcgrath is a Bitcoin and cryptocurrency enthusiast, passionate about the potential these tools and blockchain technology bring to the world and writes consistently for CoinReview. He has been following the development of blockchain for several years. To know his work and more details you can follow him on Twitter @McgrathStevan.

See full profile

![How to Create a Budget for BI & Analytics Services [With Template]](https://img.shgstatic.com/clutch-static-prod/image/resize/715x400/s3fs-public/article/f07e9d6bd89e7f70df9c94301acdd847.png)