How Executive Search Firms Help Fast-Growing Companies Build Leadership Teams That Scale

Avoid costly executive hiring mistakes. Learn how search firms help B2B companies hire leaders who deliver results.

Updated April 1, 2026

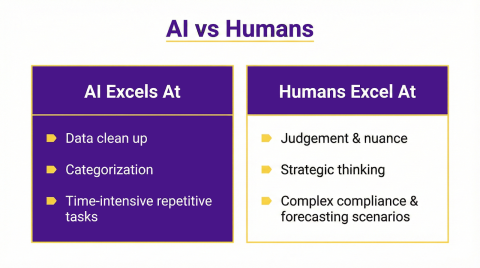

Where does AI excel? Where is human oversight needed? And what does a human + AI financial services model look like?

Tools that once struggled to count the number of r’s in strawberry are now helping with forecasting, scenario planning, and automating workflows that used to take days to complete.

So, it’s no surprise business owners are wondering:

Looking for a BPO agency?

Compare our list of top BPO companies near you

As AI improves, do we still need accountants, bookkeepers, and CFOs?

This article provides insights from indinero, a full-stack accounting, tax, bookkeeping, fractional CFO, and payroll service provider.

Things that used to take junior professionals days are being handled by a single skilled AI user in a matter of hours. Data cleaning, transaction categorization, and month-end reconciliations can be automated in ways that were impossible just a few years ago.

“I had ChatGPT review a tax return for me the other day,” shares indinero Senior Tax Director, Brian Miller. “And I’ll be honest, it did a pretty good job.”

AI performs best in deterministic environments. Places where rules are consistent, you feed it quality first-hand data, and include a detailed prompt with clear explanations of what to (and not) to do.

Used correctly, it’s a powerful accelerator for financial operators.

But speed isn’t the same as accuracy.

Remember the attorneys who submitted ChatGPT-generated briefs citing made-up cases? It didn’t happen just once, and all across the country, they’re being sanctioned and fined tens of thousands of dollars for their transgressions.

We have to remember: AI is just fancy autocomplete. It’s not thinking. And you can’t trust its answers without double-checking everything. Indinero tax director had ChatGPT review a return, yes. But the only reason he knew it did a good job is because he has the background to understand a “good job” in the first place.

“The tools do their best,” indinero senior director of business development, Tyson Yoon, says. “But if you don’t put down the perfect prompt and keep a keen eye out for hallucinations, it’s probably not going to be very good.”

Hallucinations aside, another concern is AI’s probabilistic nature. It’s trained to predict the most statistically likely word in a sequence, and uses a randomizer to choose from there. But in finance, “almost correct” isn’t correct at all.

A 1% drift in a revenue forecast over several years could be the difference between solvency and crisis. And if you’re trying to sell a business? Small deviations in assumptions could mean leaving tens or hundreds of thousands of dollars on the table.

Trusting AI to completely take the reins is risky. It’s useful for automating financial processes, but it can’t replace expertise, judgement, or experience.

Tax law, payroll rules, and reporting standards can be complicated in the best of times, let alone after a recent rule change.

AI models hallucinate, and even when they provide accurate information, they may still rely on outdated training data. It’s impossible to know if what it shares is reliable.

New credits and deductions are introduced every year. Old deductions are phased out. Thresholds change. States reinterpret nexus rules. And agencies may issue new guidance that subtly alters how rules are enforced, even if the underlying statute hasn’t changed.

If something goes wrong, the IRS isn’t going to take “the model told me so” for an answer. Even as technology improves, businesses may still need experienced professionals to protect them from potentially costly mistakes.

One of the most important, and perhaps frustrating, roles of a CFO is knowing when to say no.

AI is helpful. Give it a prompt, and it will do its best to produce a plausible answer. But if those assumptions are overly optimistic or incomplete, the output will reinforce a decision that may turn out to be costly.

And that’s before considering, sometimes, you just don’t know what you don’t know. If you don’t think to prompt AI with the right question, there could be crucial blind spots in the strategy you develop.

Human advisors bring context, experience, and judgment to the table. They’ve seen what happens when companies expand too quickly, take on the wrong kind of debt, or chase revenue at the expense of cash flow.

If we have to push back? We will, where AI won’t.

Garbage in? Garbage out.

If the books are messy, inconsistent, or incomplete, ChatGPT can only automate the confusion. Financial models need well-structured data, with cleanly organized expenses, revenue, and strategic planning inputs, to succeed.

Maybe ChatGPT can oversee an already well-designed accounting system. But it certainly can’t build one. It’s still worthwhile to incorporate human oversight over AI-automated workflows.

Entrepreneurs wear plenty of hats, especially in startups and small businesses. But sometimes, you’d rather have someone with specialized expertise handle things for you.

It’s the same reason most of us don’t change our own oil – we have better things to do.

And yes, absolutely. Most business owners could take the time to critically evaluate whether an AI-generated forecast is realistic or not. They’re incredibly talented individuals, and they could check into the latest tax rules to make sure ChatGPT really uncovered a hidden deduction, or if it was misinterpreting rules in a way that could land you in hot water.

But do you really want to?

Sometimes, it’s nice to just call someone and get an answer. “What’s our monthly cash flow? We’re trying to get a loan. The bank needs to know. We’re thinking of making a hire, could you check the math and make sure we can afford it? We don’t want to overextend.”

Would you trust ChatGPT with your tax return? Even though you’re on the hook with the IRS for any mistakes? Probably not, and we wouldn’t either.

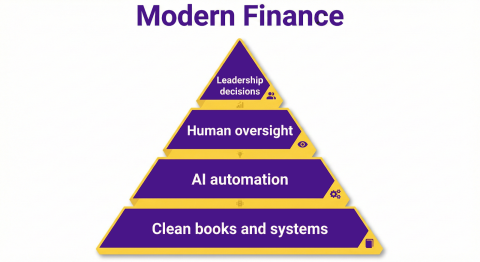

In our view, trying to completely replace humans with technology isn’t a winning formula. Duolingo tried, and since announcing in April they were becoming an “AI-first” company, their stock price crashed by ~70%. We believe the real sweet spot is combining AI efficiency with expert oversight.

AI handles the mechanical work.

Data extraction, cleanup, reconciliation, month-end workflows.

Humans handle the strategic work.

Setting and testing assumptions, ensuring compliance, adapting to evolving legislation, and providing forward-looking insights that shape a company’s future.

The AI revolution looks a lot more like how computers transformed accounting in the 90s than the ‘robots are taking all the jobs’ apocalypse people predicted when ChatGPT was released. Just as spreadsheets replaced pen and paper, data shows workers are adapting, upskilling, and thriving.

Tyson puts it plainly:

“We actually use ChatGPT ourselves. Automating some of our processes saves clients money. But AI can only create the foundation. There’s a lot of assumptions and manual adjustments you need to make.”

Instead of being replaced, financial professionals are offloading low-value repetitive tasks, leaving more space for the analysis and strategic thinking we went to school for in the first place.

![How to Create a Corporate Training Budget [With Template]](https://img.shgstatic.com/clutch-static-prod/image/resize/715x400/s3fs-public/article/f8cb0a8fb8e36a14ff257e02ce8b9475.jpg)