5 Tips for Small Businesses Filing Their Taxes

Tax season is right around the corner — partnerships, LLCs, and S-Corporations are expected to file by March 14, 2024, while C-Corporations have until...

Updated February 24, 2026

During the COVID-19 pandemic, 40% of Americans have been worried about their financial investing. To alleviate stress during this uncertain time, Americans should build money management skills and figure out which money mistakes to avoid.

Does the idea of looking at your bank account cause a sense of dread? Does the ping of your banking app make you question every single one of your spending choices?

You are not alone.

Looking for a Accounting agency?

Compare our list of top Accounting companies near you

APA’s recent Stress in America study found that 72% of Americans felt stressed about money at least once in the last month.

While many high school math classes are filled with theorems, shapes, and algebraic equations, basic life skills are not on the syllabus.

Money management is defined as “the process of budgeting, saving, investing, spending or otherwise overseeing the capital usage of an individual group.”

As consumers are exposed to a wide range of financial resources and plans, figuring out how to spend money wisely and build money management skills can be a challenge.

Many start with investing for the future – but as the coronavirus pandemic affects the banking and financial industries, some Americans are unsure where to start when it comes to money management.

40% of Americans are worried about their financial investments during the pandemic.

As this concern lingers, some Americans lack confidence in their money management practices and are making money mistakes. We surveyed 501 Americans about their investment habit and money management skills over the past year.

Your money management journey starts with finding the right inspiration. Just make sure that dream is within your means.

More than half of Americans (52%) are focused on investing in retirement plans.

Outside of retirement, Americans are saving their money to pay down debts (6%), purchase homes (4%), invest in education (3%), and plan weddings (2%).

Pericles Rellas is a prosperity coach at Abundance & Prosperity. He encourages people to live lives of power, purpose, and prosperity, which includes managing their relationship with money.

“Each of us has a unique set of circumstances that should be taken into consideration before choosing what to do with your money,” Rellas said. “The bottom line is know where you stand financially and create where you want to be in five, 10, or 25 years in the future.”

“The bottom line is know where you stand financially and create where you want to be in five, 10, or 25 years in the future.”

Once you know what your money is going, it’s easier to put a plan in place.

Experts say that to begin, people should prioritize simple wins:

Throughout this experience, it is important to remember that prioritizing initial success will make your goal seem more achievable.

Having a budget is crucial to managing money effectively.

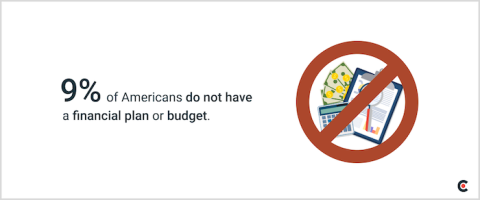

About 1 in 10 Americans (9%) do not have a financial plan or budget.

Budgets keep track of expenses, help keep people out of debt, and help people organize their financial priorities.

Aaron Simmons, founder of TestPrepGenie.com, an education blog, spent years figuring out money management. After trial and error, he is proud of his plan.

“To save more money, the most important thing to do is to cut out unnecessary expenses, stick to a foolproof budget, and don’t deprive yourself of fun too much,” Simmons said.

A clear, well-defined budget makes spending easy.

To begin, list out your expenses and track your spending. Once the grunt work is finished, budgeters can begin to use their personal systems to their advantage.

Andrew Aran is a managing partner at Regency Wealth Management, a financial services consultancy.

“A plan allows you to work towards a goal and monitor progress towards it,” Aran said. “It needs to be specific yet flexible as life happens.”

It is important to note that budgets can change over time. The first budget you create will not be the one you’ll have forever.

First-timers must commit to staying consistent with budgeting while understanding that budgets are designed to change over time.

A simple swipe can do more harm than good.

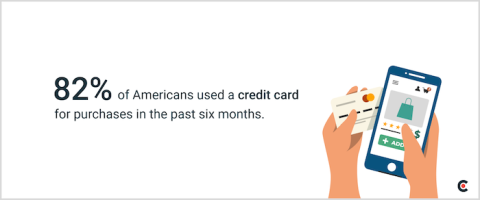

In the past six months, 82% of Americans used a credit card for their purchases.

Only 18% never used a credit card in the last several months.

According to WalletHub, the average American household has over $7,000 in credit card debt.

How do Americans have so much credit card debt?

There is a psychology behind credit card spending. Since consumers aren’t spending “real” money, they’re more likely to make use of their plastic cards. The bill that comes at the end of the month is in the back of their minds.

Studies have also shown that consumers are more willing to spend more when charging their purchases, making them the prime source of spending for impulse buyers.

To combat your excessive swiping, try out these tips:

If you’re mindful about your credit card purchases, they can become a resourceful tool during your financial journey.

A goal for expert money managers is to grow wealth and stability through financial security.

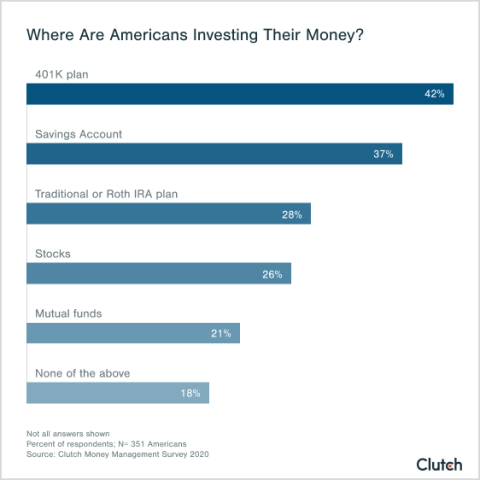

Saving and investing money in different channels allows Americans to achieve financial security. Experts say it is especially important that people contribute to savings accounts which nearly 4 in 10 Americans (37%) already do.

Currently, Americans use a range of other options to invest their money, including 401K plans (42%), Traditional or Roth individual retirement accounts (IRAs) (28%), stocks (26%), and mutual funds (21%).

Experts believe that savings accounts are the best place to start investing and managing money.

“A savings account is important because it is the backstop for your financial life,” said Ashley Agnew, the associate director of relationship development at Centerpoint Advisors, a wealth and investment firm. “A healthy savings account will give you the confidence to make better investment decisions.”

“A savings account is important because it is the backstop for your financial life."

Experts say that opening a savings account is a key aspect of being financially independent. It is important to set aside money each month. For example, taking a small percentage out of your paycheck is an easy and simple way to get started.

“It is the safest, most risk-free approach to living your life in comfort,” said Philip Ash, founder of Pro Paint Corner, a painting advice service.

For the majority of his career, Ash worked in finance. When Ash graduated from college 30 years ago, he stopped his house painting business. Years later, he used his money management savvy and savings to found Pro Paint Corner, which indulges his passion for home renovation and gives him a break from all the numbers.

By saving, many workers can achieve financial security and stability and pursue their dreams.

Overall, consistent saving allows people to meet their money management goals.

To put all of your money management skills to use, you must be consistent.

People who have successful saving habits stick to their goals and only change them when life events such as pay raises and career changes occur.

Stacey Hyde, a CPA at Envision Financial Planning, a financial services provider, believes that consistency is the best money management strategy.

“A financial plan is simply a guide,” Hyde said. “You’re stating where you want to go.”

“A financial plan is simply a guide."

Hyde’s advice is to update your financial plan every few years while charting your progress to see how far you’ve come.

Without consistency, it is easy for money management beginners to fall back into old habits or make money mistakes.

A common mistake Americans make is not having a set financial plan.

Not having a financial plan leads to bigger financial risks. Without a financial plan, people are more likely to be unprepared for unexpected surprises.

This can also cause impulsive buying decisions.

“If you don’t know where your money is going each month, then you are more likely to rack up debt and create bigger financial problems for yourself,” said Rebecca Hunter, the CEO of The Loaded Pig, a personal finance website.

“If you don’t know where your money is going each month, then you are more likely to rack up debt and create bigger financial problems for yourself."

The first step to overcome a delayed financial plan is knowing where to start, which means evaluating your spending habits.

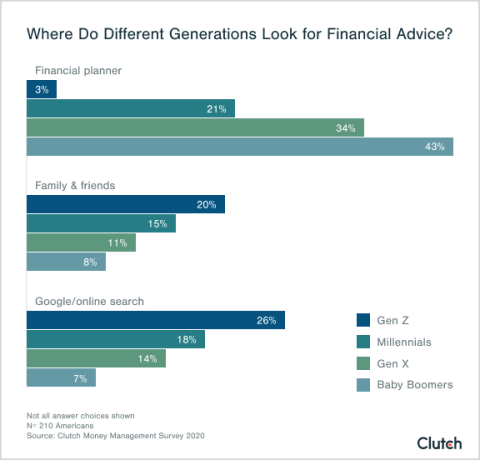

People use different financial planning resources to determine the best plan.

Across different generations, Americans use different resources for their financial decisions. Baby Boomers (43%) rely on financial planners, while nearly 30% of Gen Zers use Google and online searches for their financial advice.

Younger generations are more likely to rely on online resources and news for their financial guidance, while older generations are more likely to invest in a personal connection with a financial advisor.

Regardless of what financial planning tool you choose, having a financial plan in place is essential.

Using shiny credit cards for every purchase can lead spenders down a dull path.

Studies show that consumers are more likely to spend with their credit cards than cash.

Vanessa Gordon is the publisher of East End Taste Magazine, a lifestyle publication.

While Gordon owns five credit cards, she sets goals to spend less than $50 at least 3 days per week. Like most Americans, she uses her cards for food, travel, personal shopping, and select bills.

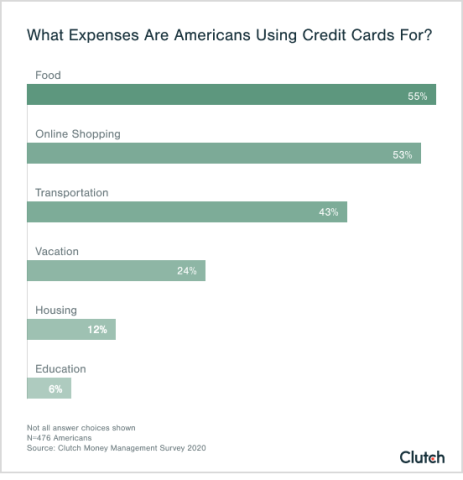

In the past six months, Americans most frequently used their credit cards for food purchases (55%) and online shopping for items such as self-care items and clothing (53%).

The temptation to overspend is hard to ignore. Beyond that, credit cards aren’t the easiest currency to understand.

If a user doesn’t understand the fees, how are they able to figure out how excessive spending impacts their credit score?

“Many cards will open with a low-to-no interest rate, but quickly jump once the promotional period is over,” Agnew said. “With a swipe or online entry, the debt obligation disappears until the following billing cycle, when it is easy to ignore or forget.”

To fight the urge for excessive credit card use, set hard boundaries for using your credit card.

“I’m aware of what our credit card statements are on a daily basis,” Gordon said. “As long as you have control of your spending daily, you’ll remain confident.”

“As long as you have control of your spending daily, you’ll remain confident.”

The way to best protect yourself is to use your credit cards on what you truly need – not a new pair of sweatpants.

If you let payments pile up, it only hurts in the long run. But the coronavirus pandemic has made it more difficult for people to stay on top of their payments.

“A lot of people don’t have a safety net right now,” Bruce McClary, the vice president of communications at the National Foundation for Credit Counseling, told NBC News. “About 40% of all Americans don’t have enough savings to cover a $400 emergency. What are they going to do if they have weeks of reduced work or no work at all?”

This time of economic turmoil hasn’t helped with financial anxiety.

As many Americans await relief from the government, all bills and payments become a priority, which can create an ever-growing list of expenses.

“If you can develop good money hygiene, it makes life so much easier,” Hyde said. “If you don’t have to think about saving, you’re much more likely to stick to it. We only have so much mental energy.”

Don’t overthink when due dates come along. Instead, set up automatic payments to take off some pressure.

Having money management skills allows people to prepare for these situations, no matter how intimidating they might seem.

Navigating the world of money management can be intimidating. Whether it is starting out with a financial plan or the daunting task of performing math, beginners need somewhere to start to build up their money management skills.

Start with setting financial goals that are realistic and work well within a budget.

Once a budget is in place, it is important to remain consistent and think of where to invest your money beyond your checking account.

Avoid overspending with credit cards by setting limits and staying on top of payments.

Putting these recommendations into action will assist money management beginners and help them avoid money mistakes.

Clutch surveyed 501 Americans in November 2020 to learn about how they spend and manage their money.

50% of respondents identify as male; 37% as female; 13% didn’t identify their gender.

Baby boomers and older make up 30% of respondents; Generation Xers make up 26%; millennials make up 15%, and Generation Z makes up 7%. 22% of respondents didn’t reveal their age.

Respondents are from the Midwest (34%), South (31%), West (24%), and Northeast (12%).